Just half of all sterling-denominated funds have survived the past decade, according to research.

Of the funds in existence on January 1 2021, one in two are still active, said S&P’s Index Versus Active scorecard.

The sector with the highest number of closed funds is Europe Equity, with 40 per cent of funds still active today.

Conversely, 60 per cent of funds in the UK Small Cap Equity sector are still running.

Percentage of sterling denominated open-ended funds still in existence

Category | Benchmark | 1y | 3y | 5y | 10y |

Europe Equity | S&P Europe 350 | 93 | 79 | 64 | 40 |

Europe ex-UK Equity | S&P Europe Ex-UK BMI | 92 | 78 | 73 | 52 |

UK Equity | S&P United Kingdom BMI | 95 | 84 | 75 | 49 |

UK Large/Mid Cap Equity | S&P United Kingdom LargeMidCap | 93 | 78 | 67 | 45 |

UK Small Cap Equity | S&P United Kingdom SmallCap | 98 | 94 | 87 | 60 |

Global Equity | S&P Global 1200 | 94 | 81 | 71 | 50 |

Emerging Market Equity | S&P/IFCI Composite | 97 | 81 | 73 | 51 |

US Equity | S&P 500 | 96 | 84 | 72 | 47 |

Source: S&P

Matt Brennan, head of investment management at AJ Bell, said this is “staggering”, given most funds tell investors they should invest in them for at least five years.

“Not all funds will have disappeared altogether, with several of them merging into other funds, however as an investor in an active fund, the question perhaps shouldn’t be ‘will this fund beat the benchmark’, but rather ‘will it still exist in the long term?”

Fees vs size

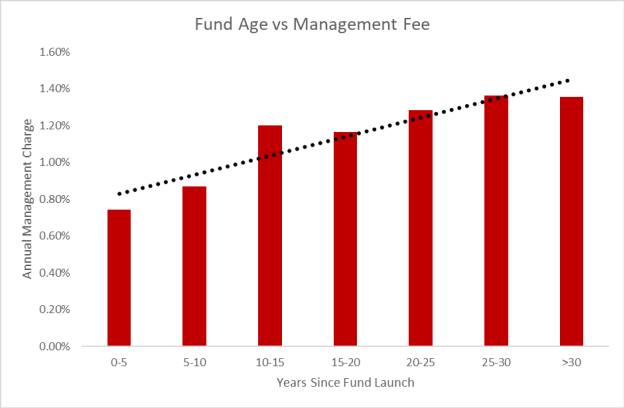

Analysis by AJ Bell showed that of the 640 open-ended active sterling-denominated funds with a 10-year track record, assets under management for each fund was was £725mn on average.

For those with less than 10-years’ track record, the average asset size is 30 per cent lower at £510mn.

AJ Bell outlined the “surprising” ongoing cost of funds for the former were almost 50 per cent higher than the latter, sitting at 1.38 per cent and 0.93 per cent respectively.

Source: Morningstar, AJ Bell, March 2022

Brennan said this shows that despite being larger in size, a fund with a long, successful track record can charge a premium for its management.

This is regardless of the fact that they are operating larger funds on average.

“Or a less generous interpretation would be that older funds which have built a large investor base are sitting on their laurels, and letting inertia take its course,” he said.

“On the flip side of the coin, newer funds need to offer lower costs to be competitive against incumbents, and to compete against passive funds.

“These dynamics perhaps point to why there hasn’t been as much of a squeeze on active fund management fees as many expected.”

sally.hickey@ft.com